There are many young people debating whether they should renew the lease on their apartment or sign a contract to purchase their first home.

Housing Cost & Net Worth

Whether you rent or buy, you have a monthly housing cost.

As a buyer, you are paying YOUR mortgage.

Every mortgage payment is a form of what Harvard University’s Joint Center for Housing Studies calls “forced savings.”

“Since many people have trouble saving and have to make a housing payment one way or the other, owning a home can overcome people’s tendency to defer savings to another day.”

The principal portion of your mortgage payment helps build your net worth through building the equity you have in your home.

As a renter, you are paying YOUR LANDLORD’S mortgage.

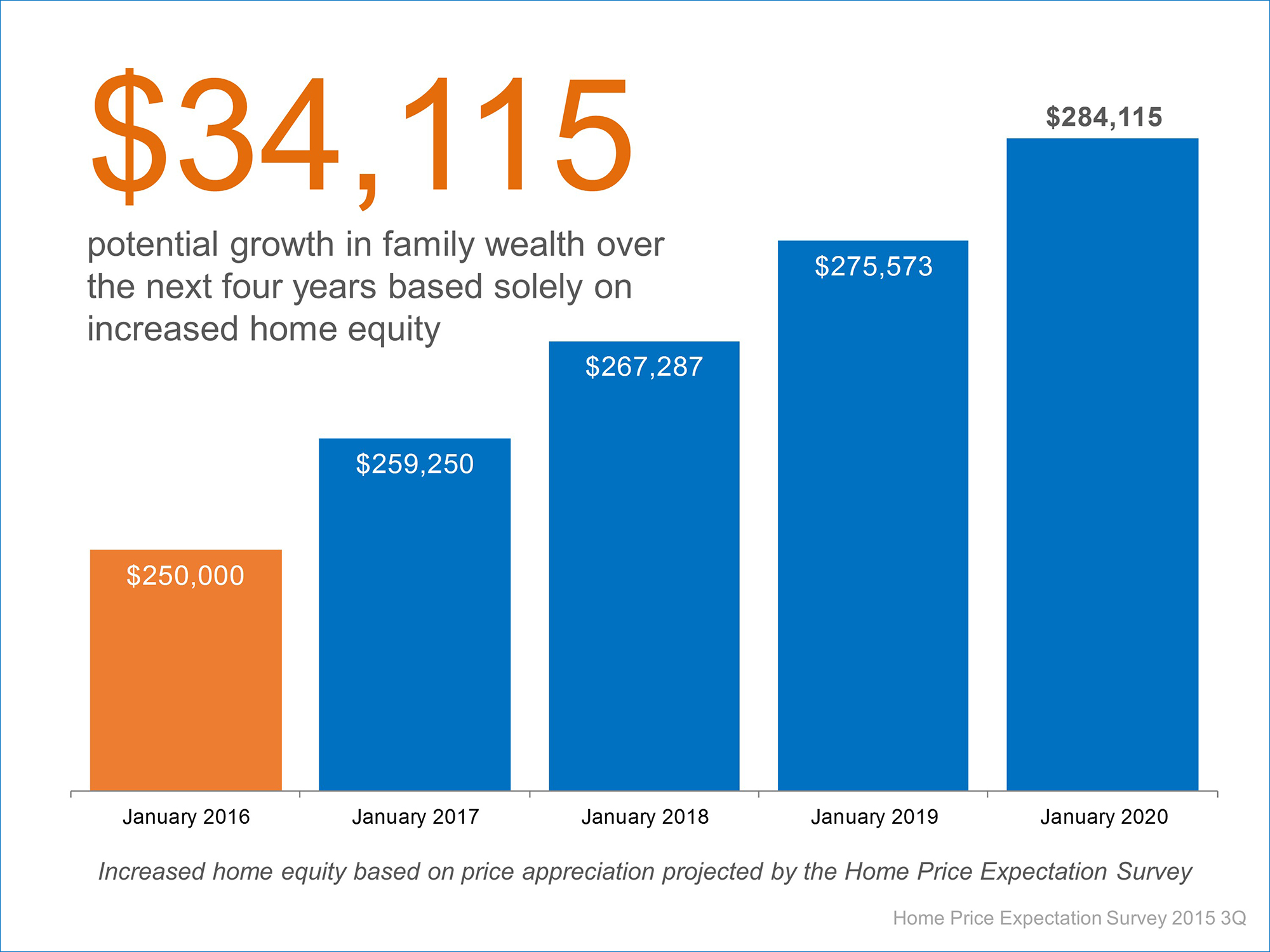

Below is an example of the home equity that would be accrued over the course of the next four years if you were to buy a home by the end of this year; based on the results of the Home Price Expectation Survey.

In this example, simply by paying your mortgage, you have just increased your net worth by over $34,000!

Bottom Line

Use your monthly housing cost to your advantage! Let's get together and discuss the opportunities available in our market.